Blockchain technology has become one of the most revolutionary innovations in the digital world. From cryptocurrencies to supply chain management, it is transforming how data is stored, verified, and shared. But many people still find it confusing. So, let’s break it down in simple terms and understand how blockchain works step-by-step, along with real-life examples.

What is Blockchain? (Quick Overview)

Before diving into the steps, let’s understand the basic idea.

A blockchain is a distributed digital ledger that records transactions across multiple computers in a secure and transparent way. Instead of storing data in one central place, it is shared across a network, making it almost impossible to hack or manipulate.

Think of it like a digital notebook that is copied and shared with thousands of people. Every time a new transaction is written, everyone gets updated, and no one can secretly change it.

Key Components of Blockchain

To understand how blockchain works, you should know its main parts:

- Block – A container that stores transaction data

- Chain – Blocks linked together in sequence

- Nodes – Computers that maintain the blockchain network

- Miners/Validators – People or systems that verify transactions

- Consensus Mechanism – Rules used to agree on transactions

Step-by-Step Process of How Blockchain Works

Let’s go through the complete process step-by-step.

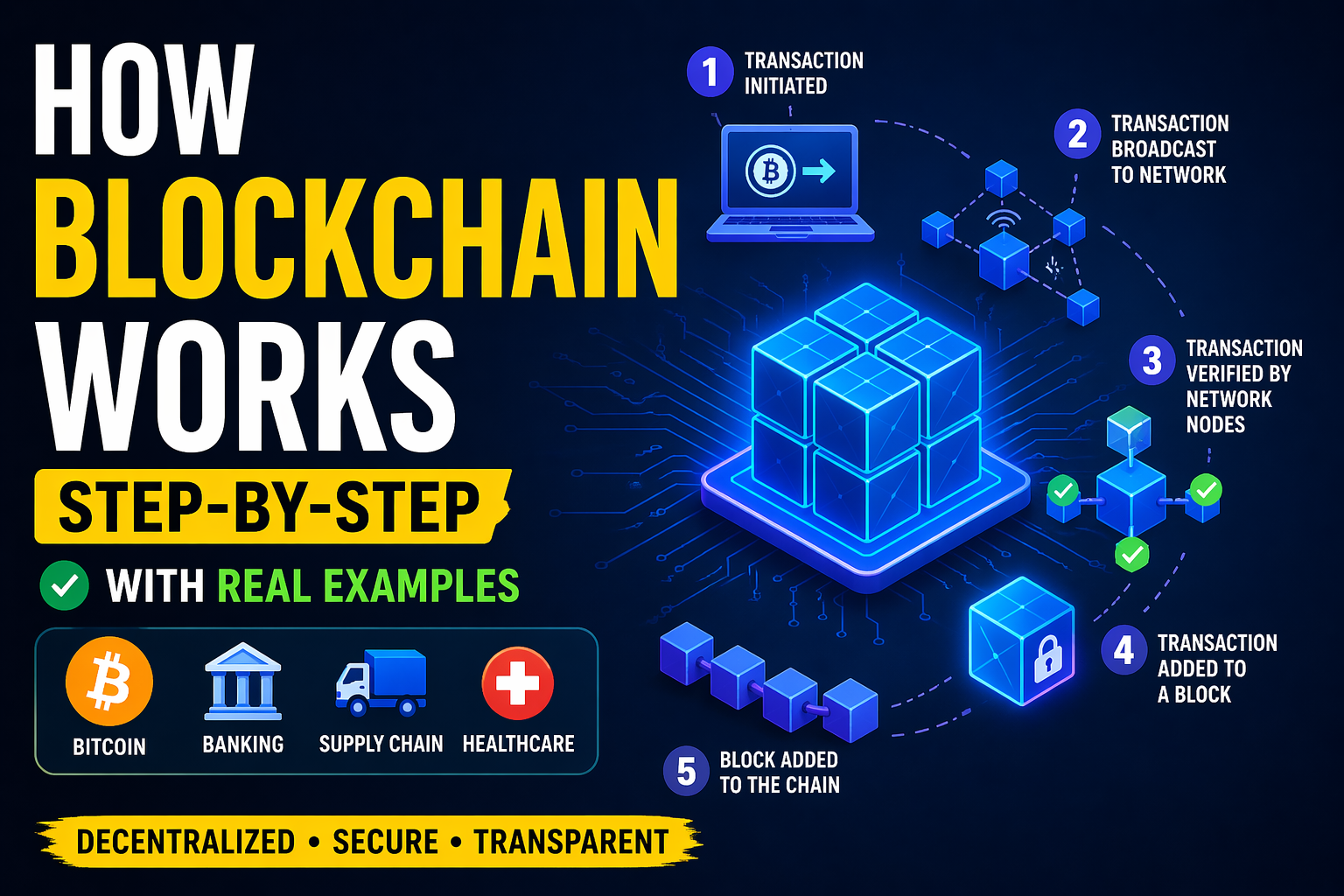

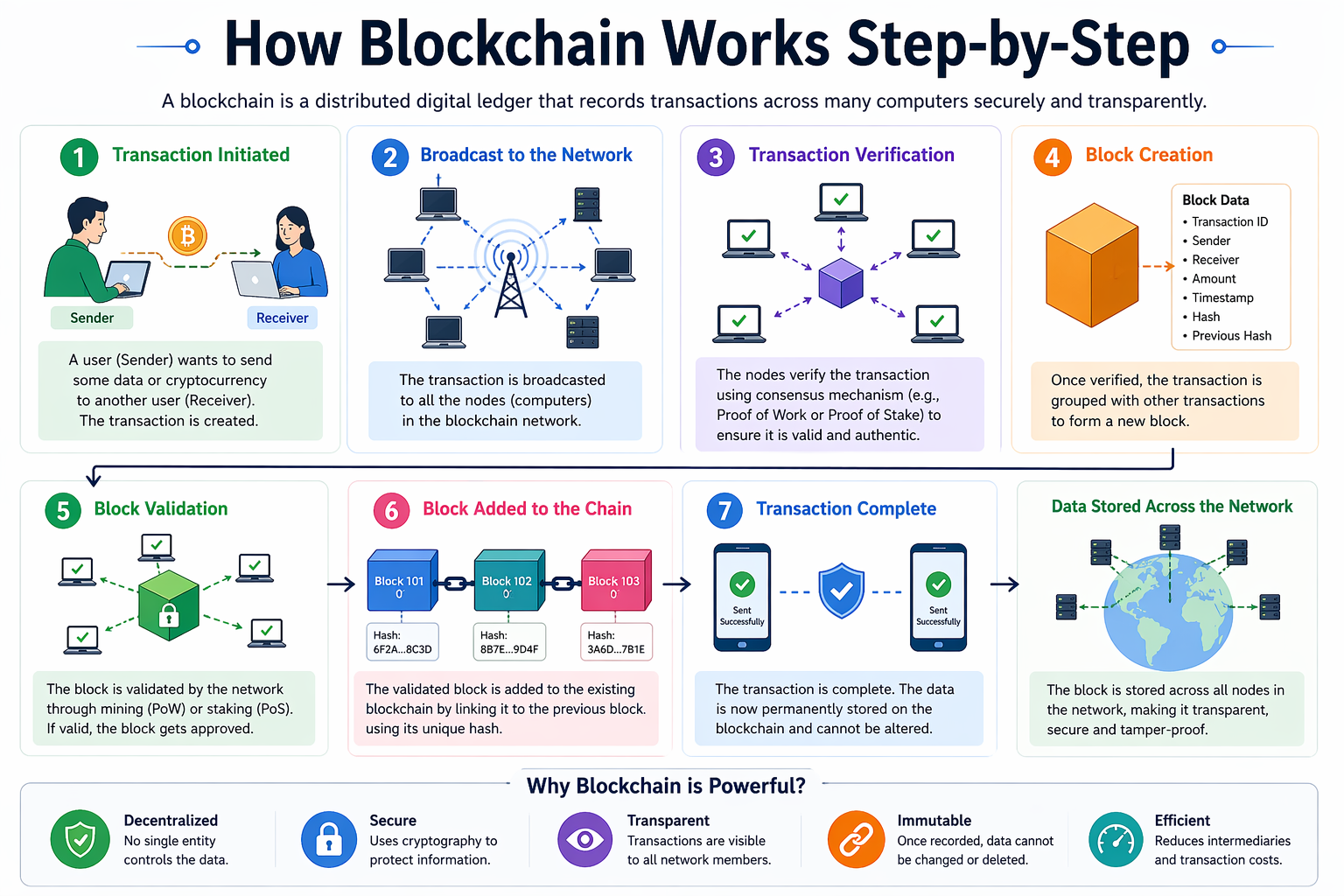

Step 1: A Transaction is Initiated

Everything starts when someone makes a transaction.

For example:

Sudhir wants to send ₹1000 to Shubham using cryptocurrency.

This transaction includes:

- Sender’s details

- Receiver’s details

- Amount

- Timestamp

The transaction is then created digitally and sent to the blockchain network.

Step 2: Transaction is Broadcast to the Network

Once the transaction is created, it is broadcasted to a network of computers (nodes).

These nodes are spread across the world and work together to process the transaction. This makes blockchain decentralized, meaning no single authority controls it.

Step 3: Transaction Verification Begins

Now, the nodes verify whether the transaction is valid.

They check:

- Does Rahul have enough balance?

- Is the transaction authentic?

- Is there any attempt of fraud or double-spending?

This verification process depends on the consensus mechanism, such as:

- Proof of Work (PoW)

- Proof of Stake (PoS)

Step 4: Transaction is Added to a Block

Once verified, the transaction is grouped with other transactions into a block.

A block contains:

- List of transactions

- Timestamp

- Unique identifier (hash)

- Previous block’s hash

This is where blockchain becomes powerful—each block is linked to the previous one.

Step 5: Block is Validated by the Network

Before adding the block to the chain, it must be validated.

In some systems (like Bitcoin), miners solve complex mathematical problems to validate the block. This process is called mining.

In other systems (like Ethereum 2.0), validators are chosen based on their stake.

Once validated, the block is ready to be added to the blockchain.

Step 6: Block is Added to the Blockchain

After validation, the block is added to the existing blockchain.

Now:

- The transaction becomes permanent

- It cannot be changed or deleted

- Everyone in the network gets updated

This creates a transparent and tamper-proof record.

Step 7: Transaction is Completed

Finally, the transaction is completed.

Rahul has successfully sent ₹1000 to Amit, and the record is permanently stored in the blockchain.

Real-Life Example of Blockchain Working

Let’s understand this with a real-world example.

Example: Sending Cryptocurrency

- You send Bitcoin to your friend

- The transaction is broadcast to the network

- Nodes verify the transaction

- It gets added to a block

- The block is validated by miners

- The block is added to the blockchain

- Your friend receives the Bitcoin

This entire process happens within minutes and without any bank involvement.

Why Blockchain is Secure

Blockchain is considered highly secure because of the following reasons:

1. Decentralization

Data is not stored in one place, making hacking extremely difficult.

2. Cryptography

Each transaction is encrypted using advanced cryptographic techniques.

3. Immutability

Once data is added, it cannot be changed.

4. Transparency

All transactions are visible to network participants.

Advantages of Blockchain

- High Security

- Transparency

- No Middleman Required

- Fast Transactions

- Reduced Costs

Limitations of Blockchain

While powerful, blockchain also has some challenges:

- Scalability Issues

- High Energy Consumption (PoW)

- Regulatory Uncertainty

- Complex Technology

Future of Blockchain

Blockchain is not just about cryptocurrency anymore. It is being used in:

- Banking and Finance

- Healthcare

- Supply Chain

- Voting Systems

- Real Estate

In the future, blockchain could become a core part of digital infrastructure across industries.

It was a amazing network I really like this