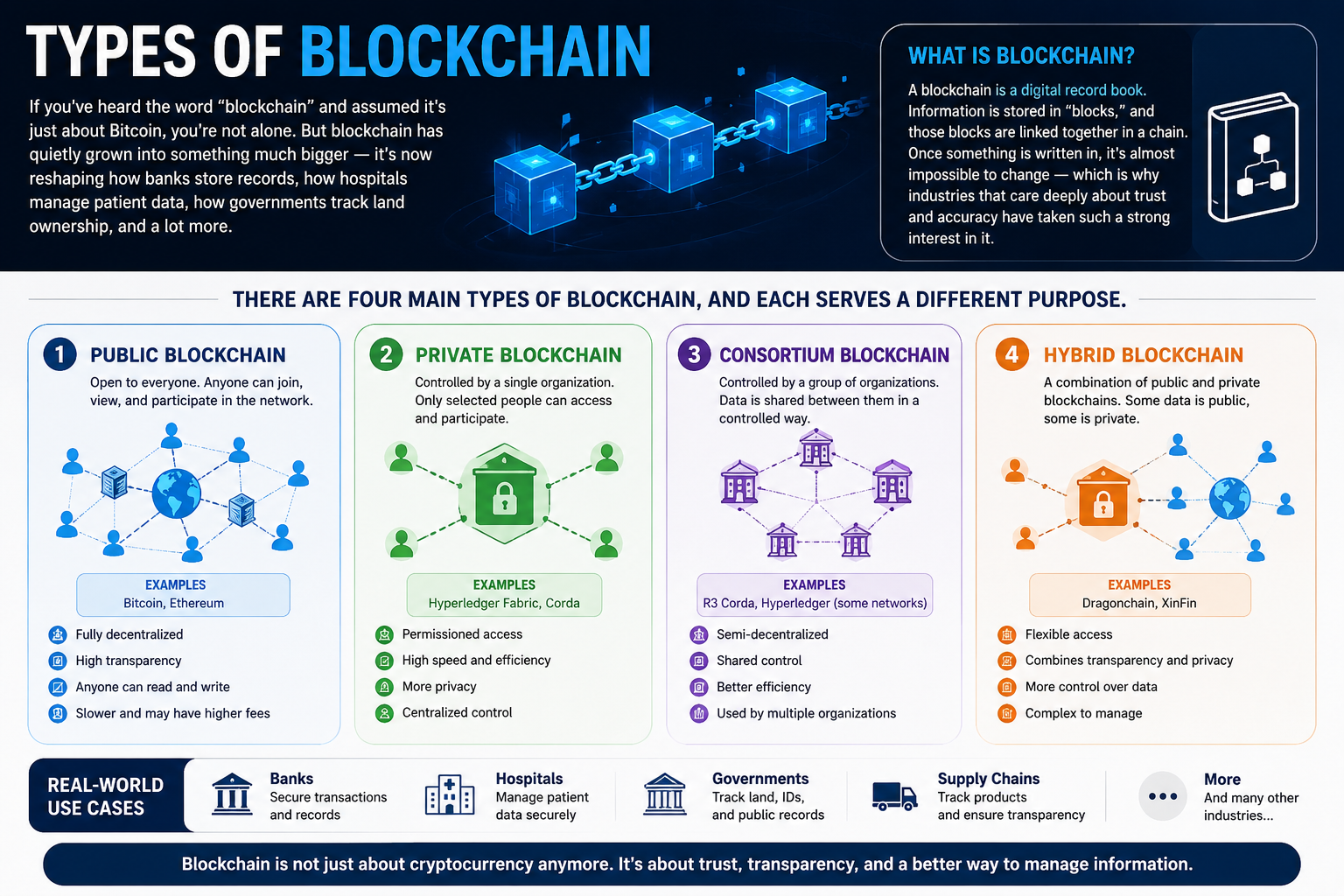

If you’ve heard the word “blockchain” and assumed it’s just about Bitcoin, you’re not alone. Most people make that connection. But blockchain has quietly grown into something much bigger — it’s now reshaping how banks store records, how hospitals manage patient data, how governments track land ownership, and a lot more.

At its core, a blockchain is really just a digital record book. Information gets stored in “blocks,” and those blocks are linked together in a chain. What makes it special is that once something is written in, it’s almost impossible to change — which is why industries that care deeply about trust and accuracy have taken such a strong interest in it.

But here’s something most people don’t realize: there isn’t just one type of blockchain. There are actually four main varieties, and each one serves a pretty different purpose. Let’s walk through them.

1. Public Blockchain — Open to Everyone

Think of a public blockchain like a giant open noticeboard in a town square. Anyone can walk up, read what’s there, and add their own message. No one owns it, no one controls it, and everyone can see everything.

Bitcoin and Ethereum are the most well-known examples. Thousands of computers around the world (called “nodes”) keep the network running and verify every single transaction.

What’s great about it: The openness is exactly what makes it trustworthy. You don’t have to rely on any company or government — the system itself does the checking. It’s also extremely difficult to hack because there’s no single point of weakness.

The trade-offs: That openness comes at a cost. Processing transactions takes time because so many nodes need to agree. Bitcoin’s verification system also guzzles a lot of electricity. And as more people join, things can slow down even further.

Where it’s used: Cryptocurrency transfers, decentralized apps, digital voting systems, and crowdfunding platforms.

2. Private Blockchain — For Organizations That Need Control

Now imagine that same noticeboard — but it’s locked inside a company’s office. Only employees with a badge can get in, and the company decides exactly who can read or write anything.

That’s essentially what a private blockchain is. One organization runs the show. Platforms like Hyperledger and R3 Corda are built for exactly this kind of use.

What’s great about it: Because fewer computers are involved, transactions happen much faster. Sensitive data stays protected. And the organization can scale things up or down as needed without much fuss.

The trade-offs: You’re trusting one organization completely. If they decide to manipulate data internally, there’s not much stopping them. And since it’s not open, outsiders have no way to verify what’s happening.

Where it’s used: Internal banking systems, employee records, healthcare data, business contracts, supply chain tracking within a single company.

3. Consortium Blockchain — When Multiple Organizations Share Control

This one sits in interesting territory. What if several hospitals, or a group of banks, all wanted to share a blockchain — but none of them wanted any single one to be fully in charge?

That’s a consortium blockchain. A defined group of organizations jointly manages the network. Each participant has a role, and no single party can override the others. It’s semi-decentralized — more open than a private blockchain, but more controlled than a public one.

What’s great about it: It’s built for collaboration. The costs and responsibilities are shared, security is stronger because multiple parties are watching, and transactions are faster than on a fully public chain.

The trade-offs: Getting multiple organizations to agree on rules and governance is genuinely complicated. Disputes can arise. And since access is still restricted, transparency is limited to participating members.

Where it’s used: Banking networks, insurance groups, collaborative supply chains, joint government projects, and research consortiums.

4. Hybrid Blockchain — The Best of Both Worlds

Some situations are complicated. An organization might want certain data to be completely public and verifiable — while keeping other data private and protected. A hybrid blockchain makes this possible.

You get to choose: this information goes public, that information stays locked. It’s flexible in a way the other types aren’t.

What’s great about it: Businesses get real control over their data without having to sacrifice transparency entirely. It’s also faster than a purely public chain and more cost-effective than running separate systems.

The trade-offs: Designing a hybrid system is complex. Users have to trust the organization managing the private side — which reintroduces some of the same concerns as a private blockchain.

Where it’s used: Real estate transactions, government service portals, retail businesses, healthcare management, and financial institutions that need to balance privacy with public accountability.

Quick Comparison

| Feature | Public | Private | Consortium | Hybrid |

|---|---|---|---|---|

| Who can join | Anyone | Invited only | Selected group | Controlled |

| Who’s in charge | No one (decentralized) | One organization | Multiple orgs | Mixed |

| Transparency | High | Low | Medium | Selective |

| Speed | Slower | Fast | Fast | Fast |

| Security | Very high | High | High | High |

| Cost | Higher | Lower | Shared | Moderate |

So Which One Actually Matters?

The honest answer is: it depends entirely on what you’re trying to do.

If you’re building something that needs to be open, verifiable, and free from any central authority — a public blockchain makes sense. If you’re a company that just wants to improve internal record-keeping with better security — a private blockchain is probably the right fit. If you’re part of an industry where multiple players need to share data but none should dominate — consortium is the model to look at. And if your needs are somewhere in the middle, hybrid gives you that flexibility.

Where Is All This Heading?

Blockchain is still maturing, but it’s moving fast. Countries including India are exploring it for everything from land registries to education certificates to digital identity systems. Developers are also weaving it together with AI, IoT, and the emerging Web3 ecosystem.

None of the four types is “winning” — they’re each evolving for different niches. What’s clear is that blockchain isn’t just a cryptocurrency thing anymore. It’s becoming part of the infrastructure that modern digital life runs on.

And understanding the difference between these four types is a solid starting point for anyone who wants to follow where it’s going.